基本概念

邊際貢獻

邊際貢獻邊際貢獻是管理會計中一個經常使用的十分重要的概念,它是指銷售收入減去變動成本後的餘額,邊際貢獻是運用盈虧分析原理,進行產品生產決策的一個十分重要指標。通常,邊際貢獻又稱為“邊際利潤”或“貢獻毛益”等。

作用

邊際貢獻

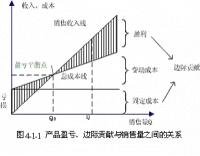

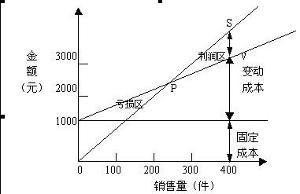

邊際貢獻在產品銷售過程中,一定量的品種邊際貢獻首先是用來彌補企業生產經營活動所發生的固定成本總額,在彌補了企業所發生的所有固定成本後,如有多餘,才能構成企業的利潤。這就有可能出現以下三種情況:

(1) 當提供的品種邊際貢獻剛好等於所發生的固定成本總額時,企業只能保本,即做到不盈不虧。

(2) 當提供的品種邊際貢獻小於所發生的固定成本總額時,企業就要發生虧損。

(3) 當提供的品種邊際貢獻大於所發生的固定成本總額時,企業將會盈利。

因此,品種邊際貢獻的實質所反映的就是產品為企業盈利所能作出的貢獻大小,只有當產品銷售達到一定的數量後,所得品種邊際貢獻才有可能彌補所發生的固定成本總額,為企業盈利作貢獻。

國際會計英語中稱為contribution margin。

A cost accounting concept that allows a company to determine the profitability of individual products.

It is calculated as follows:

Product Revenue - Product Variable Costs

Product Revenue

The phrase "contribution margin" can also refer to a per unit measure of a product's gross operating margin, calculated simply as the product's price minus its total variable costs.

Consider a situation in which a business manager determines that a particular product has a 35% contribution margin, which is below that of other products in the company's product line. This figure can then be used to determine whether variable costs for that product can be reduced, or if the price of the end product could be increased.

If these options are unattractive, the manager may decide to drop the unprofitable product in order to produce an alternate product with a higher contribution margin.